Manufacturers appear to be committed. They have planned more capacity increases and are bound and determined to fill that capacity with more sales – no matter what the level of incentives.

This approach has gone beyond marketing du jour; it has become a marketing pillar. Yikes! That marketing strategy sounds all too familiar.

Financing deals and incentives continue to push light-vehicle sales beyond what economic and employment growth would dictate, by about 300,000 units.

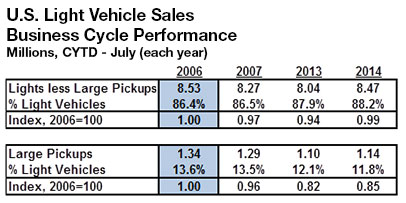

However, even with incentives, the 2014 monthly sales have not been able to match comparable 2006 sales levels, a key benchmark year when volumes reached 16.5 million units and economic fundamentals were stronger.

July’s sales performance is indicative of what has been happening all year. Deliveries for all models other than large pickups stood at 99% of the like-2006 performance; large pickups alone performed at 85%, a relatively poor showing.

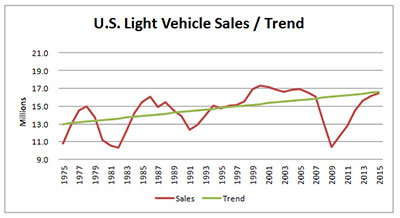

If the market is going to hit a bigger stride, and finish higher than 16.2 million for 2014, it has to put up numbers that are at least 105% of the 2006 benchmark.

The average seasonally adjusted annual rate for this year provides guidance the 2014 market will come in at 16.1 million units, with the last four months averaging a robust 16.6 million. Can it go further and hit the 16.5 million trend line?

It depends. The opportunity for the light-vehicle market to perform above 16.5 million-unit trend line in the current business cycle is very limited if we just look at economic fundamentals. Looking back to 1975, we can see how light-vehicle sales have performed against the estimated trend each year.

It depends. The opportunity for the light-vehicle market to perform above 16.5 million-unit trend line in the current business cycle is very limited if we just look at economic fundamentals. Looking back to 1975, we can see how light-vehicle sales have performed against the estimated trend each year.

From 1975 to 2000, every year light-vehicle sales were at or above the estimated trend line combined gross domestic product and employment growth was in excess of 5.2% – a big number compared with 2014’s 3.8%.

From 1975 to 2000, every year light-vehicle sales were at or above the estimated trend line combined gross domestic product and employment growth was in excess of 5.2% – a big number compared with 2014’s 3.8%.

During the post-9/11 period there were some exceptions to this fundamental relationship. During 2001-2005, when the prime rate averaged about 5% and the housing boom was under way, sales performed above trend even with GDP and employment growth registering a paltry 2.7%. (Note: Sales declined each year from 2001-2003, although were above trend).

The bottom line: Manufacturers will need incentives to keep the market growing. Even with the optimistic estimate of 4.5% combined GDP and employment growth for 2015, it appears as if a 3.25% prime rate is the best hope for continued market expansion. Otherwise, the peak is at hand.

Suppliers interested in quantifying their 2015 opportunities would be advised to keep one eye on the prime rate and the other on actual sales performance versus the 2006 benchmark.

Warren P. Browne is president of WP Browne Consulting and has extensive experience in the global automobile industry. During the past 20 years, he has held senior executive positions at General Motors, including in Brazil, Poland and Russia. He currently serves as an adjunct professor of economics at Lawrence Technological University.