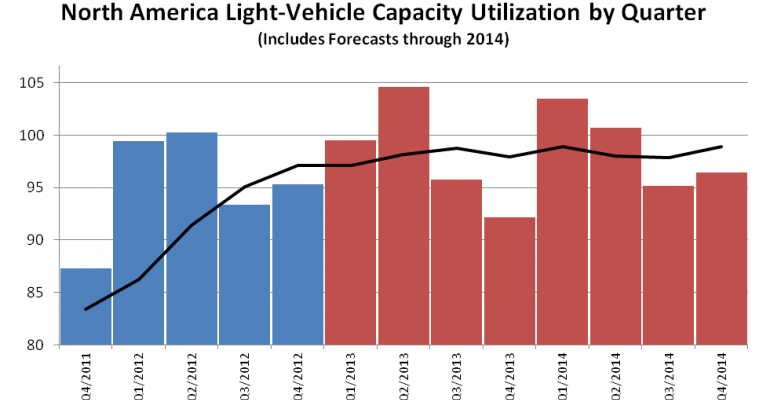

Rising demand and inventory catch-up, resulting in more overtime and a proliferation of plants working 3-shift or 3-crew schedules, led North American light-vehicle manufacturers to build to 97.1% of their 2-shift straight-time capacity in 2012, based on a WardsAuto analysis.

It was the highest rate since WardsAuto began tracking the data in 2005, well above 2011’s 83.4%, and the most recent trough year of 2009, when manufacturers built to just 51.9% of their capacity.

By country, capacity utilization soared to 124.0% in Mexico in 2012, up from robust totals of 111.4% in 2011 and 102.6% in 2010.

Capacity utilization in Canada reached 99.6% in 2012, compared with 80.2% the prior year. A 15.5% increase in production and one fewer plant in the system with the closure of a Ford operation in late 2011 mainly were responsible for the gain.

Auto makers in the U.S., which accounted for about two-thirds of 2012 North American output, had strong capacity utilization last year at 91.0%, up from 78.2% in 2011.

Fourth-quarter 2012 capacity utilization was 95.3%, compared with like-2011’s 87.3%. Nearly all manufacturers recorded higher rates than year-ago except the Ford/Mazda joint venture assembly plant in Flat Rock, MI, and Subaru Indiana, which assembles Subarus and Toyota Camrys.

Several manufacturers, most with a high mix of plants running 3-shift/3-crew schedules and including Ford, Hyundai, Kia, Nissan, and Volkswagen, had utilization rates above 100% in the fourth quarter.

As might be expected with demand pushing plants past their straight-time limits, manufacturers increased their available production mainly through the addition of third shifts and crews, as well as by improving the 2-shift capabilities at some facilities.

For light vehicles, available production (defined as installed straight-time capacity including third shifts/crews, less downtime for vacation, holidays and long-term retooling for new products) increased by 842,000 units in 2012 from prior-year to 15.6 million. The 2012 total was the highest since 16.4 million in 2007.

Even with the increase, North American manufacturers pushed the envelope by building to 97.8% of their available production, well above 2011’s 88.5%.

The 2012 increase mostly was generated by a gain of 875,000 units in the U.S. from 2011 to 10.5 million. Mexico chipped in another 48,000 and it, combined with the U.S., more than offset a decline of 81,000 in Canada.