U.S. light-vehicle sales as expected topped a 15 million annual rate for the first time in years last month, in part a result of a bounce-back from October when Hurricane Sandy took a chunk out of demand.

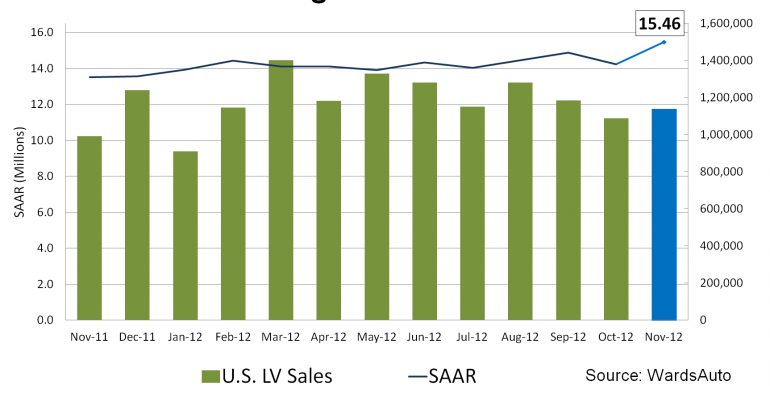

Sales marched upward to a 15.5 million seasonally adjusted annual rate, the first time since March 2008 the SAAR topped 15 million and the highest since the same total in February 2008.

The performance also was well above October’s 14.2 million and year-ago’s 13.5 million and brought the year-to-date SAAR to 14.3 million, compared with 12.6 million for 11-months 2011.

WardsAuto still anticipates 2012 to end with sales of 14.4 million, but there’s a chance the industry will hit the 14.5 million mark.

Auto makers confirm some sales were delayed from October in November, but add that replacement volume of vehicles damaged in the hurricane was not a significant factor in last month’s performance.

Ford estimates 20,000 to 30,000 industry sales in November were carried over from the prior month. Analysts from both Ford and GM expect replacement volume to begin in earnest this month and continue through the end of next year, but with the biggest impact in December and the early months of 2013.

November volume of 1.139 million units equaled a daily selling rate of 45,565, 14.9% above year-ago’s 39,650 – 25 selling days both periods. It was the 27th-straight increase. Year-to-date 2012 sales totaled 13.089 million, 13.9% above 11-months 2011’s 11.495 million.

Even though this time of year usually favors large trucks, the mix continued to trend toward cars.

Sales of large pickups increased only 8.0% from year-ago, and share for the segment declined to 11.5% from 12.2% in like-2011. Demand for large SUVs dropped a whopping 18.0% from year-ago and market share fell to 1.9% from 2.7%.

Commensurate with that trend was a 13.0% drop in large cross/utility vehicle deliveries.

However, sales of Middle, Middle Luxury and Large Luxury CUVs more than offset the Large CUV downturn, giving the entire CUV group a 14.8% gain. Notably, Small CUVs were up only 6.3%.

Light-truck deliveries increased 9.3%, while cars were up a robust 21.6% from year-ago.

The strongest segment groups were Small Cars, up 32.6%, and Middle Cars, with an increase of 15.6%.

Nearly all manufacturers recorded year-over-year gains in November.

Market leader General Motors recorded a lukewarm 3.4% rise, while its market share declined to 16.4% from the prior month’s 18.0% and year-ago’s 18.2%.

Ford also posted a below industry-average gain, with sales rising 5.8%. Its market share increased from the prior month to 15.2%, but was well below year-ago’s 16.5%. Lack of inventory for the ramping-up new Ford Fusion caught some of the blame.

The remaining manufacturers among the top six in volume all outpaced the industry average.

Honda sales surged 38.9%, bringing its to-date increase to 23.8%. Its market share of 10.2% improved on the prior month’s 9.8% and was well above year-ago’s 8.5%.

No. 3 Toyota’s 17.2% increase was good for a 14.2% penetration, which was above year-ago’s 13.9% but below its 11-month 2012 share of 14.4%.

Chrysler had its 32nd straight year-over-year gain with a 14.4% jump in sales. Increases posted by the Dodge and Ram brands offset a 3.3% decline at Jeep, its second straight after 29 consecutive increases. The Chrysler brand posted a relatively flat November, although to-date deliveries were up 43.1%.

Rounding out the top six, Nissan rebounded from two consecutive downturns to a 12.9% rise in November, though its market share dropped to 8.4% from like-2011’s 8.6%.

Among other manufacturers, Volkswagen/Audi’s huge gain of 28.0% in November actually brought its to-date increase down to 30.7%. However, its market share of 4.4% was its highest of the year and best since before 1980.

Other manufacturers recording November gains were Hyundai (7.8%), Kia (10.9%), Mazda (17.7%), Suzuki (21.7%) and Volvo (26.8%). Posting declines were Isuzu, Tata and Mitsubishi.