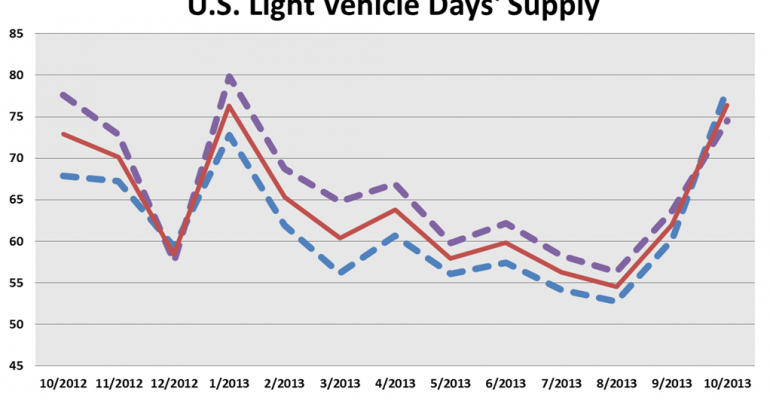

With the government shutdown playing a role, October U.S. light-vehicle inventory jumped to long-times highs for the month in both volume and days’ supply.

There are extenuating circumstances that explain the highs, but the levels harken back to early in last decade when steep price discounting was used to prop volumes, keeping annual U.S. LV sales well above trend.

Excluding 2008 when the industry was heading into recession, LV inventory totaled 3.397 million at the end of October, highest for the month since 3.803 million in 2004. October’s 76-day supply, was the highest for the month since 77 in 2005.

By comparison, sales in 2013 mostly have run at highs dating to 2007, suggesting inventory is getting ahead of the curve.

The days’ supply stands out because it exceeds the 75 days’ October averaged from 2002 through 2005, a period when annual U.S. sales averaged 16.8 million units. The year-to-date 2013 seasonally adjusted annual rate through October is 15.4 million.

There are three main reasons why inventory climbed to a 9-year high.

First, the Thanksgiving holiday is in the final weekend of the month, meaning Monday, Dec. 2, will count in this month’s final sales tally. This fluke of the calendar has occurred only twice in the previous 10 years and will result in higher raw volume.

Second, lost sales caused by the government shutdown in October led to slightly higher inventory at the end of the month. WardsAuto estimates it added two days to October’s days’ supply. The excess will be alleviated in November, when most of the lost sales are recouped.

Finally, demand is in a strong growth period. Since recording a 15.3 million SAAR in first-quarter 2013, highest since the final three months of 2007, the quarterly SAAR has increased by 200,000 units from the previous 3-month period in both the second and third quarters to 15.5 million and 15.7 million, respectively. WardsAuto expects the fourth quarter to continue the pattern and post a 15.9 million-unit SAAR.

Thus, it makes sense for inventory to climb ahead of the curve to meet rising demand.

November’s SAAR likely will spike upward from October, possibly close to 16 million units. December is likely to hit the same level, with a good chance of going higher.

The downside is that inventory now is bordering on excess for the first time in several years.

If demand in the final two months of 2013 falls short of expectations, that, coupled with the forecasted 14-year-high fourth-quarter North American production, could mean some trimming to early 2014 schedules.

If sales fail to rebound in the first three weeks of November, odds are good for enhanced holiday deals that largely continue into December, starting a surge that would last through year’s end.

November’s days’ supply usually stays flat with October, but this month’s extended sales period should push the daily selling rate higher and lower days’ supply from October.

Expect something in the 60-to-65 days’ range at the end of December.

October’s inventory was 11.4% higher than year-ago’s 3.049 million, and days’ supply was higher than October 2012’s 73. However, similar to this year, October 2012’s inventory was jacked up due to unusual circumstances.

Hurricane Sandy blasted the East Coast in October last year, and culled an estimated 50,000 to 60,000 units from the month’s sales. Accordingly, days’ supply temporarily spiked upward.

Oct. 31 inventory of domestically produced LVs totaled 2.75 million, 10.6% above year-ago. Days’ supply totaled 80, compared with 76 a year ago, and an increase of 15 days from the prior month, the same September-to-October increase as in like-2012.

Import inventory totaled 648,676, 14.8% above year-ago and equal to a 64 days’ supply. Except for 2008, it was the highest October import days’ supply since 72 in 1995.

Much of the import buildup is in CUVs, a long-term growth segment, and luxury cars, which typically have strong market shares in the fourth quarter. Based on their car inventory levels, the Audi, BMW, Infiniti, Jaguar and Porsche brands are expecting strong finishes to 2013.