Investment: n. the investing of money or capital in order to gain profitable returns, as interest, income, or appreciation in value.

Detroit Three automakers will face brutal investment requirements over the next five years to maintain competitiveness in North America.

These requirements have exploded beyond the traditional bending of sheet metal and boring of holes in engine blocks.

Against this cash-drain backdrop, risk factors also are exploding. Arguably, environmental risk has never been higher, given the uncertain outcome of NAFTA talks and final carbon-dioxide emissions standards.

The overall automobile business also is getting riskier. Yes, light trucks are paying their way. But payback on everything else – sedans and coupes, electric and hybrid vehicles and safety, connected and autonomous vehicles – looks scary for the Detroit Three.

Somebody ultimately has to pay for all this stuff, and at this stage it is not clear that it will be consumers. Suppliers beware.

Just when some industry analysts were starting to get worried, a cash benefactor came to the rescue: the U.S. government. The new corporate tax law, lowering the nominal rate from 35% to 21%, ultimately will provide added cash to development spending and capital budgets. That’s great. Yet, the tax change will do nothing to change the risk factors.

Prior to the 2009 recession, manufacturers had to primarily worry about establishing a balanced vehicle portfolio for the wide-ranging demands of the market. No small task, given fickle consumers and a wide variance in oil prices. Recall that companies went broke attempting to serve those fickle consumers.

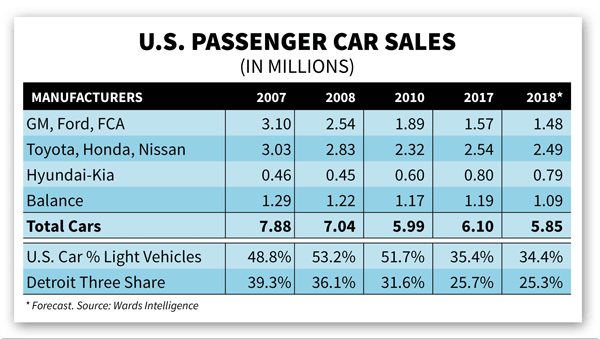

Manufacturers always have known that U.S. car sales have been more cyclical than light trucks. Since 1960, car sales have decreased when trucks have increased 16 times – mostly in years with weak economic growth. Rarely do car sales go up when trucks go down.

This variability has become much more severe in the last three years. Cars captured a meager 35.4% of light-vehicle sales in 2017, the lowest level ever. Result: Car sales have fallen 1.78 million units in just a decade.

However, the car catastrophe is not industry-wide. The Detroit Three account for 86% of the decline. Eliminating the negative effects of discontinued dinosaur divisions such as Mercury, Saab and Pontiac does not alter the conclusion: Detroit Three car sales have plummeted – even with an increase in the number of models offered.

Concurrently, Asian brands continue to dominate the top 30 car models. This premier group has maintained sales within 2% of levels established in 2007.

For the Detroit Three, keeping the overall light-vehicle portfolio competitive over the next decade will consume considerable capital. There’s nothing new there. However, allocating the right amount of capital between cars and trucks has become much riskier for them – a situation Asian and European makes are avoiding.

From our previous analysis posted by WardsAuto, we know major car improvements don’t always lead to sales success. So, the Detroit Three face a risk multiplier: More car models to improve coupled with declining share and volume. Something’s got to give.

Electric/Hybrid Development Multiplies Car Risk

The risk is even higher in other areas of the automobile business. In the good old days, engineers and product planners just had to worry about annual minor and major program improvements, including powertrains. Over the past decade, complexity, workload and incremental spending have increased with the advent of alternative powertrain vehicles: hybrids, fuel cell and electrics.

Currently, electric-only and hybrid vehicles don’t fall into the “products we gotta have” sales quadrant – for any manufacturer. Sure, they are the darlings of the public relations and press community, but they are not selling and they don’t appear to be making any money.

According to WardsAuto data, there are approximately 77 electric/hybrid models in the light-vehicle market, with 20 being introduced in 2017 alone (there were deletions as well). Yet, deliveries have flat-lined at a paltry 3% of the market. Increased sales from Ford’s Fusion, Toyota RAV4, Toyota Highlander and the new Kia Niro and Chevrolet Bolt kept overall sales in this sub-segment from declining. Even the mighty Tesla S underperformed. The top six models generate half the business; the rest sell in embarrassingly low volumes given the level of engineering work and money spent. Spoiler alert: 2018 sales do not look any better.

Oh, but that’s not stopping electric-vehicle dreamers. Detroit Three planners are looking for even more capital by offering more promises and hope. Manufacturers are tripping over themselves to announce more electric/hybrid vehicles and paint a very rosy picture of the future (where everything always looks brighter). To hedge their bets, they also are lobbying for reduced CO2 emission standards in the U.S. and Europe. What happens to electric-vehicle demand if all the lobbying efforts to reduce emissions standards produce results?

Hopefully, manufacturers are not waiting for a gallon of gas to cost $4.50, my estimate of the national average required to push U.S. electric/hybrid sales above 15% of the market, or to generate a level of price/value consumers actually recognize. Unfortunately, that level of gasoline price would provoke a serious sales decline for cash-rich light trucks.

China, France and the U.K are helping maintain enthusiasm with government-mandated solutions. But can manufacturers really wait for 2030 to earn a return? In the U.S., let’s hope the Trump infrastructure proposal allocates significant money for charging stations in all 50 states. Maybe global prices for the core raw materials for batteries will just fall. Don’t bet on it. Consequently, electric/hybrid vehicles are just near-term cash burners banking on government-mandated demand and subsidies.

Autonomous Vehicles Pile On Risk

But the risk gets multiplied again with autonomous vehicles. The Detroit Three, seemingly shaken by the automotive juggernauts Google and Tesla, are spending cash to develop a self-driving vehicle for fleets. A fleet-only introduction will allow them to generate small-volume failures and experience – the hallmark of any innovation activity. That makes sense.

Selling self-driving vehicles to individual consumers is a long way off despite the daily hoopla. Profitable sales may be even further down the road. Do consumers really want this level of driving inflexibility? Are they willing to pay for the redundancy costs, or insurance cost increases? Forecasts about future demand have been published; none of them had a consumer price tag associated with them. This should be a red flag for any corporate treasurer.

Autonomous-vehicle development is engineering-push at its finest, goaded by automotive writers who can’t wait to report on the latest widget that went 20 miles (32 km) without a crash. Isn’t driving the best part of owning a performance car? Somehow, I can’t imagine an advertising slogan that proclaims “the ultimate self-driving machine.”

The highest level of value for individual consumers seems to be technologies that help avoid front-to-rear collisions at all speeds, the most common type of auto accident in the U.S. For individual consumers, the Detroit Three should just install full-braking systems in all vehicles and call it a day. That appears to have the biggest investment payback. Likewise, keep automated development to a single vehicle until consumers indicate they actually will pay for all the cost. Keep it simple.

That brings me back to the title of this article. U.S. corporate tax cuts have become a long-term white knight for cash-hungry planners looking to add complexity. Unfortunately, hope-based assumptions are enabling more engineering cost and capital spending above historical business requirements, without demonstrated customer needs being identified.

Tax cuts will provide the Detroit Three with serious incremental cash to develop the future; that’s a good thing. Yet, the significant risk permeating the current automotive environment can’t be disguised by bold proclamations about what will happen in five or 10 years.

Warren P. Browne is an adjunct professor of economics at Lawrence Technological University. He retired as a GM executive in 2009 and formed his own automotive consulting company.