Auto makers selling in the U.S. market would be wise to use per-gallon gasoline prices of up to $4.25 in their product-planning assumptions, says a leading oil-industry analyst who also advises higher costs are possible.

“Overreactions can breed episodes at $4.50-$5.00,” says Tom Kloza, chief oil analyst for the Oil Price Information Service, a New Jersey-based data tracker. “I do not, however, concur with some folks who believe that we may see $5.00 gasoline by (the end of) 2012.”

Kloza’s remarks come on the heels of a forecast by a former Shell Oil Co. president John Hofmeister, who now heads a grassroots lobby called Citizens for Affordable Energy. Hofmeister warns of $5.00 per-gallon regular-grade prices in 2012 accompanied by “blackouts, brownouts, gas lines (and) rationing.”

Such dire predictions, made during an interview with the independent TV news show, Platts Energy Week, are enough to send chills through a recession-weakened U.S. auto industry struggling to regain its footing.

But there is little evidence on the showroom floor that the $3.00-per-gallon threshold – breached just days ago for the first time since 2008, according to the American Automobile Assn. – is spreading panic.

When pump prices hit their all-time record of $4.11 in mid-2008, there was a “tremendous” wave of change, says Michael Perrault, general manager of Vista Mini in Coconut Creek, FL.

Consumer behavior skewed rapidly and dramatically, Perrault tells Ward’s, as he recalls the parade of Hummer and Cadillac SUVs he accepted as trade-ins at his lot just north of Ft. Lauderdale.

“As of now, I have not seen a mad rush,” he says. “I think $4.00 is the threshold.”

Auto makers are generally mum on details of their planning assumptions. But there is ample proof they regard $4.00 gasoline as a certainty.

General Motors Co.’s pre-bankruptcy viability statement filed with Congress anticipates the price jump by 2014.

Chrysler Group LLC, as it existed in the DaimlerChrysler AG era, expected $4.00 as early as 2010.

Not surprisingly, the industry now is seeing a relative flood of fuel-efficient vehicles ranging from the gasoline-powered Fiat 500 A-segment minicar arriving in dealerships in first-quarter 2011, to the all-electric Nissan Leaf compact that bowed earlier this month.

A Ward’s analysis of the U.S.-market product cycle through model-year ’12 shows 14 electrified vehicles and 17 small and minicars in the pipeline.

Related document: North America Product Cycle Chart, 2007-2016

“The real key is timing,” says Pete Delongchamps, vice president-manufacturer relations at Group 1 Automotive, which oversees nearly 100 U.S. new-vehicle dealerships.

Detroit OEMs were guilty of doing too little too late in 2008, while Toyota Motor Co. was prepared with the thrifty Prius hybrid, Delongchamps says.

The U.S. Energy Information Admin.’s short-term energy outlook calls for $3.00 gas in 2011. So are OEMs doing too much too soon today?

“The consumer is not going to be afraid of $3.00 gas,” says Michigan-based auto industry consultant Jim Bulin. “They’re not going to change their buying habits. They know (gas) can go down as easily as it can go up.”

Says Kloza: “I would think that we’ll see slightly softer prices about five weeks from now, and then a climb toward $3.25-$3.75 (per gallon) in spring.”

“After that period, it will depend on world economic growth, but retail gasoline prices often peak in May and then spend the rest of the year backing off a bit from those numbers,” Kloza adds.

The national average per-gallon price of regular-grade gasoline is hovering near $3.07, up $0.23 in the last month, according to AAA.

Why the sudden climb? Look to the U.S. Federal Reserve, says Larry Goldstein, special projects director at Energy Policy Research Foundation Inc., a Washington-based not-for-profit organization that studies energy economics.

The Fed’s quantitative easing strategy is expanding money circulation.

“That’s designed to stimulate the economy, but what it also is designed to do is encourage investing in risk assets over fixed assets,” Goldstein tells Ward’s.

“So what we’ve seen is an influx of money by financial investors into the oil complex. Ironically, the unintended consequence of the Federal Reserve policy has driven oil prices up.”

As such, there is no simple explanation for pump price volatility. Despite increased pull in China and India, “no one country sets the price; no one supplier sets the price,” Goldstein says.

“If oil prices were simply determined by the narrow supply-and-demand in the global environment, oil prices would be materially lower than they are today.”

Therefore, the current trend of $3.00 prices, and higher, cannot be deemed the new norm.

“Because the fundamentals of the oil market really don’t justify the pump prices we’re seeing,” Goldstein says. “It’s a combination of Fed policy and financial investors.”

Even so, the market has shown resilience.

“When people are confronted with a new situation, the idea of it is a big shock,” Bulin says. “And then they find out they can live with it.”

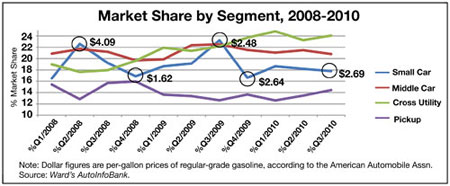

Consider the fluctuating share of small cars, as Ward’s defines the segment.

When gas prices were approaching their peak in second-quarter 2008, small cars such as the Ford Focus accounted for more than 22% of the U.S. light-vehicle market, according to Ward’s data.

By year’s end, when pump prices were less than half of what they were, small-car share plunged below 18%.

Sales jumped again following a mid-2009 gas-price hike, but fell back to 2008 levels – where they remain today – despite the steadily rising cost of gasoline.

Says Bulin “(Consumers) get fed up, initially, by gas prices. Then they sort of settle in and most people just go right back to where they were after their minds get adjusted.”

The oil crisis of the 1970s raised the specter of $3.00 gas, leading to predictions people would be “driving cars with rubber-band motors. And here we are at $3.00 a gallon and people are driving, fundamentally, the same cars they did before.”

Despite a growing number of hybrid vehicles on the U.S. market, 27 compared with 22 last calendar year, their sales through November lagged like-2009 by 7.6%, according to Ward’s.

Of OEM product-planning assumptions, Bulin adds, “I’m sure that they have contingency plans.”

As for predicting with precision the course of pump prices and their impact on new-vehicle sales: “The truth is nobody knows,” he says.

– with James M. Amend